It is the 1729th of March 2020 (aka the 23rd of November 2024)

You are 3.144.255.116,

pleased to meet you!

mailto:blog-at-heyrick-dot-eu

Nurses are revolting

Note: I worked as a Care Assistant and had quite a bit of contact with nurses, and my mother was one. So I'm probably biased here. Or maybe just not a heartless corrupt Tory bastard.

As you might have noticed from my advent videos, I'm in favour of the nurses striking. It's not just about "give us more money", although that's the primary point that the media tends to fixate upon. It's also about job security, and proper investment in the NHS as a whole. The past decade and a bit of Tory rule has suffered the NHS cutback after cutback, instead spaffing ridiculous amounts of money on failed Test&Trace schemes, dodgy PPE contracts, and trying so very hard to push as much personal medical information as possible to the American spooks.

Why?

Simple. Money. In the pockets of Ministers and primary donors. And screw all of you.

Rinse and repeat for schools and education (why teachers are striking), other emergency services (why fireman and 999 handlers are striking), the rail network (why train drivers are striking), and other public services (why binmen and civil servants are striking).

They have the quadruple whammy of Brexit (the government's own advisory estimates export losses around 15%, and gains in new exports as "negligible"), Covid (where many countries simply shut down for a while, leading to obvious economic shocks), the situation in Ukraine (causing a very real rise in the price of wheat and gas, but exacerbated by mendicious companies jumping on the bandwagon and jacking up prices "because inflation" which, in turn, causes things to cost more thus fuelling inflation), and finally the fallout of the not-budget that punched a hole (between £30 and £50 billion depending on who you ask) in the economy and badly affected interest rates which is a disaster for people with mortgages and large loans.

Note also that public sector pay freezes have meant that nurses' pay hasn't kept up with rising prices since around 2010. In real terms, what their money bought in 2022 compared to what it bought in 2010 means they have suffered a pay cut of around 10%.

What this has led to is underfunded services and underpaid and barely appreciated staff, and it's reached a point where people are saying "enough, no more". The government, for it's part, is holding firm. They would rather throw a few billion in the pockets of the board of a company they are peripherally related to (and may get a cushy non-job when they cease being MPs) than ever consider paying people fairly. Thjey aren't nicknamed The Nasty Party for nothing.

Now, I don't agree with the idea of having something like a 16-19% pay rise (I think it's supposed to be about 5% above inflation?) because what happens if and when the BoE manages to bring inflation back down to the 2-4% range? Will they be expected to take a pay cut to equalise it?

However what the government is currently offering is derisory. We all know that NHS nurses go into the job because they are (usually!) kind and caring people, not because they think it's a get rich quick scheme. However the fact that some are relying on food banks should shame the government. Public sector workers are never going to get amazing pay. French nurses' pay is pretty lousy too. But they should make enough money that they can feed themselves, heat their home responsibly (like, to ~18°C, not 26°C!), buy shoes, wash their uniforms, and pay for petrol/bus to be able to get to work...

A recent poll in the Independent shows that the public are, generally, in favour of the strike action. As well they should be. Money in the hands of the rich, especially members of the cabinet, helps nobody.

But nurses? Train drivers? Binmen? Teachers? Fireman? These are all people that various members of the general public not only expect to be there doing their job, they rely upon them doing it. The chaos in train stations as everything is cancelled demonstrates that it's something nobody cares much about until it's not there. Likewise the moderate amount of chaos in hospitals as the nurses strike (though, nurses being who they are, have been seen time and again crossing their own picket lines when people have been in genuine need of assistance) also demonstrates their importance.

Just a couple of years ago, many of them made the choice to continue working against an unknown viral infection with inadequate protection, inadequate provisions, and a workplace that rapidly turned into a miniature vision of hell with people risking their own lives both due to infection and burn-out, in order to try to help save the lives of others. They were, rightly, called heroes. People took the rather useless action of a weekly clap to demonstrate their appreciation for the fact that some people gave a shit, something the government has failed at for many years now.

But has anything changed? Quick answer - no.

That's why they are on strike, revolting against an unworkable and incoherent system and expectations.

And if you're annoyed because you are in need of a nurse and (s)he isn't there for you, just remember that they aren't doing this to hurt you. They are doing this to try to ensure that they will be there for you in the future. 34% of nurses often think of leaving, 52% feel unwell because of work related stress, and 40% feel burnt out (source: Nursing Times), while June 2021 to June 2022 saw a 25% increase in the number of nurses leaving their jobs, that's an additional 7,000 of them (source: The King's Fund) or around 40,000 in the last year (source: Nurses.co.uk). When the total number of registered nurses is around 320,000 or so, that's a rather significant amount.

It is especially rammed home by the various stories that nurses (and teaching assistants) are quitting to stack shelves in supermarkets and work in coffee shops because it pays better which allows them to, you know, pay the bills. Something that around a third of British households, a third, are struggling with this winter.

So don't get angry at the nurses. Get angry at this incompetent and corrupt government. Viva la revolution!

The Express Saving Challenge

The Express has a "saving challenge" for putting aside some money. With a big headline, they suggest that it's pretty easy to save around £7,000 in a year.

It seems so simple. Save a single fiver on the first week. For each subsequent week, add a fiver. So week two £10, week three £15 and so on.

But think ahead a little. Week forty nine would require you to save £245, in a single week. If we take weeks 49-52 (roughly the month of December), you would need to save £1,010 in that month alone. How many Express readers have that sort of money?

Especially considering the number of over 50s (the sort of people that might consider The Express to be a "real" newspaper, even though it often strays quite far from anything that resembles reality) who are on zero-hour contracts because a mixture of barely-regulated gig economy, rampant ageism, and a lack of wanting to retain unnecessary staff means that it can be hard for the over 50s to find reliable employment.

I don't read The Express, I saw this in my news feed... despite being pretty sure that it was one of my "don't show me this crap again" choices. Hmmm?

Perhaps a better approach is instead of getting people to fall for a "challenge" that seems easy at first, to instead suggest a more rational way of saving. Let's say £40 a week. Which is £160 a month. This may or may not be possible, as people have been affected by ending the £20 uplift... however it's a flat amount. The same in January as December. At the end of it, you'll have saved £1920. Which, granted, is less impressive than the aforementioned seven thousand, but it's something that's in the realm of possibility of being able to actually do. Dropping a grand into savings in December... may well not be.

Obviously, adjust the figures as per your particular situation.

Mobile phone insurance

When I got my Samsung S9... uh... about four years ago now, I think, I took out an insurance policy recommended by the guy in the Orange shop. At the time this made sense as I was holding in my hand a little gizmo with a price tag of somewhere between six and seven hundred euros.

Now you can get reconditioned ones on Amazon for about €150. Which is barely more than the yearly cost of the insurance I was paying. So it doesn't seem logical to carry on with the policy, which might even simply say no due to the age of the phone.

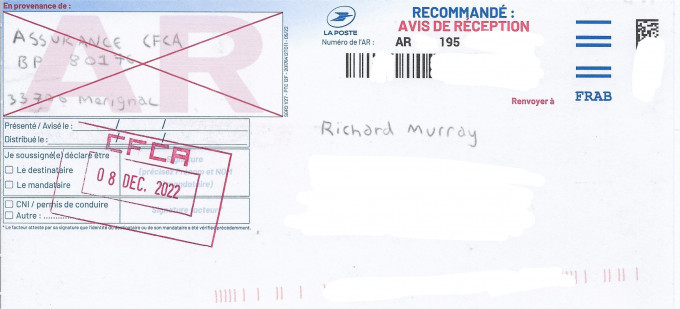

The policy was with a company called CFCA. Looking on the Internet, it would seem that this company is well known for refusing to accept contract terminations.

You might recall that I had a similar situation many years ago with my health top-up insurance, when the government introduced legislation that it was the responsibility of employers to provide such a thing for their employees. My top-up, with Suravenir (through the bank CMB) was not willing to arbitrarily cancel the insurance policy. In those days, it was quite normal for policies to automatically renew every year, with cancellation only possible during a ridiculously short period around the time of renewal.

The insurer had to begrudgingly accept my termination because employer health top up is obligatory, and you cannot have multiple top-ups.

Perhaps due to the prevalence of such arnaques (wheezes), the Loi Hamon was introduced in 2015 which stated that people were engaged to whatever policy they took out for the period of one year. After that duration had passed, they were able to terminate their policy at any timewithout penalty.

Aside: I understand that some shady insurers tried to get around this by renewing the entire policy to effectively reset the year counter back to zero. This didn't work as the debit mandate and agreement was valid for the original policy agreed to, which meant that not only was the agreement terminated on their part, they were also guilty of fraud for taking payment for a now non-existant policy.

I wrote a letter to CFCA quoting both IMEI numbers and also their payment reference. I did this as the phone line was in my mother's name back in 2019 (as the home owner), although I paid the bill and the insurance. I wasn't entirely sure whose name it was in back then. So I quoted all of the references, and knew that I would be able to cancel because I quoted the Loi Hamon (cut and paste from an online "make cancelling easy" site), though I rather expected to have to say "she died, here's a copy of the paperwork" if it was in mom's name.

Of course, it was sent registered with pingback. And that pingback duly arrived a few days later.

I knew they received it.

Imagine my surprise when, shortly after, I received the letter confirming the date of cancellation.

Cancellation confirmed.

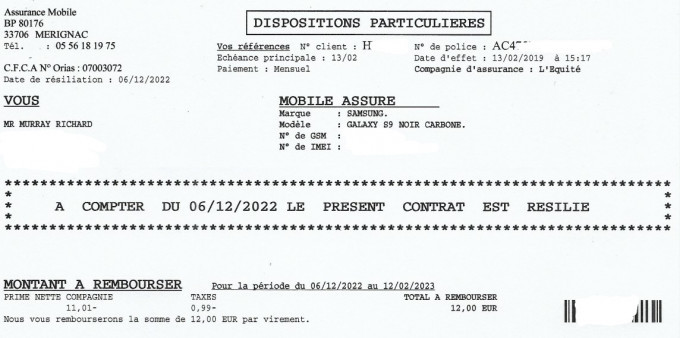

There has been no refund as yet, and €12 was taken out on the 15th of December. That's likely what the refund will be for. A covering letter stated that months in course are to be paid in full, so I effectively lose the period between the 6th (when it was cancelled) and whenever the month term ends. Mmmm, whatever. I've already 'lost' about a hundred euros due to not getting around to doing this earlier, so I'm not going to lose it over a few extra.

I'll keep a check on my bank account, and as soon as the refund arrives, I'll cancel the direct debit mandate. Just in case. ☺

And the other expenses

For my car, Felicity (!), I only have €405,34 remaining on the policy. Which means five repayments. So come May, I'll have an extra €85 each month. I could pay this off early, but in order to do this they will want to call me on a Monday-Friday between 9h and 16h45. Which is co-incidentally exactly the same hours I work. So stuff it. Just leave it ticking away in the background.

Actually, they've sent me letters every year wanting me to arrange to talk to them (within the above times) to "better discuss my needs and repayment abilities". I've ignored all of those requests for two reasons. The first is that it's when I'm at work, so no good. And the second is that the bank and I entered into an agreement. They would provide me with this amount of money (for a car) and I would repay over this number of months with this much added interest. That was the agreement. I have no need for any further discussion, thank you.

Also, I'm potentially paying slightly more interest than I would with the other bank (this loan is from La Banque Postale, the other account is with the CMB and I pretty much only keep that around to continue the home insurance and because the CMB provides a virtual credit card which is useful for online shopping). Anyway, the big mistake that the CMB did was in failing to provide a simulator. The website describes their loans, and for more information they will call you back. I do not like talking on the phone. Doubly so given that it is in French. Plus having people quote numbers and figures to a person with a mathematical inability is unfriendly and unhelpful.

The Banque Postale, on the other hand, had a simulator. Tell it how much you wanted and how long you want it for, and it'll tell you if it's a valid amount/duration, and how much monthly repayments will be. So I just threw in all sorts of values until it came to "about eighty quid" which I felt was an affordable amount for my current budget. I actually could have gone a little higher, as I expected the car insurance to cost more. But a few more months to keep the figure low is not a big problem.

Suffice to say, my first car will be finally all paid off in five months.

My various other direct debits (Instant Ink, Netflix, insurances, Internet...) add up to around €240/month. So while there is potential for belt tighteninig (the newspaper costs about €34/month, for example), I'm not worried about cashflow problems. I buy the food I want (usually pasta!) and save something each month.

To be honest, the biggest potential saving was simply dropping fast food. Sure, it was great to throw a twenty euro note in the direction of a girl wearing a cute brown uniform and silly little baseball cap in return for an enormous pile of grease and something resembling meat. But after what happened earlier in the year... I can say, hand on heart, that I have never felt pain like that before (even having my wisdom teeth yanked) and I've never puked that much in my life. Do I miss burgers? Yes. Am I going to take a chance on a repeat performance? Absolutely not. It took days for the rectal bleeding to stop, weeks for the pain to subside, and months for me to feel capable of bending down to vacuum under the lockers at work. Months. All for a twenty euro burger meal.

I don't know the cause. Bad product? Employee not washing their hands? A fly on the lettuce? Who knows. What I know is that it is relatively easy for food to be contaminated, to the point where the fact that this sort of thing doesn't happen regularly shows that - for the most part - hygiene rules are being followed. I put what happened to me down to shitty luck (with extreme emphasis on the shitty) rather than any particular failing of the place in question. But even so, I have no intention of having it happen again. Even if this means I spend the rest of my life never enjoying a jalapeño burger ever again. Oh well.

It's basically a risk assessment. Covid vaccination good, burgers bad.

Speaking of risk assessments, stay away from those non-food bins at Lidl. Full of myriad little things you never knew you needed. I bet I could drop €240/month in that place if I wasn't making a conscious effort to stay away. It's great to have one close for the must-haves (like my wall heater), but the danger lies in all the other things. If you've ever been in a Lidl, you'll know exactly what I mean and I bet the words "Parkside" and "Silvercrest" are all that need said. ☺

Your comments:

Please note that while I check this page every so often, I am not able to control what users write; therefore I disclaim all liability for unpleasant and/or infringing and/or defamatory material. Undesired content will be removed as soon as it is noticed. By leaving a comment, you agree not to post material that is illegal or in bad taste, and you should be aware that the time and your IP address are both recorded, should it be necessary to find out who you are. Oh, and don't bother trying to inline HTML. I'm not that stupid! ☺ ADDING COMMENTS DOES NOT WORK IF READING TRANSLATED VERSIONS.

You can now follow comment additions with the comment RSS feed. This is distinct from the b.log RSS feed, so you can subscribe to one or both as you wish.

David Pilling, 27th December 2022, 18:27

Yes to paying NHS staff properly and running it properly. The last nurse I spoke to was on a 12 hour shift, I'd not want to be on the receiving end of anyone who had been working for 11 hours. Anecdote is useless. Nurses are not the bottom level these days in the NHS, health care assistants are. There are lots of excellent new buildings in Blackpool NHS - a lot has been spent, might not be as much as some would want.

As for the rest, they're striking against one another. At the end all you can do is say a train driver is worth twice as much (or half, or three times) a bin man. They can also try to change their position against others or the value of assets. But it is a pie division exercise.

Two things you don't mention are the printing of money, debasing the currency via quantitative easing which went on from 2008 and into overdrive during the pandemic.

And the move to net zero. Before the war energy prices were on the rise. Virtue signalling governments, think Boris Johnson have decided on an end to fossil fuels (without providing alternatives). Hence no investment in them, hence shortages and higher prices. Renewable energy is a good thing, but there's not enough, and it has not been spelled out that it will be more expensive and as a result people will be poorer, the pie will be smaller, you can argue how it gets split up as much as you like.

There will be big winners from inflation, something the media does not mention. People with debts.

If inflation is 2% in a years time, no one will be asking for money to be handed back, prices will still be higher than they were.

J.G.Harston, 2nd January 2023, 14:32

Comparing with 2010, yes, NHS staff have gone backwards, but you're starting from a point where they'd had a decade of going forwards faster then other people. However, they do have an argument that having been put ahead of "average", they would expect to remain there.

Some of this is compounded by the "credentialisation" of the workforce. When you have people entering nursing having had to overcome the hurdle of having a degree and fifty grand of debt, instead of a couple of A levels, then the workforce reasonably expect to be paid comensurately.

J.G.Harston, 2nd January 2023, 14:33

"There will be big winners from inflation, something the media does not mention. People with debts."

<i>Look like I picked the wrong decade to pay off my mortgage.</i>

Rick, 11th January 2023, 08:04

The insurance reimbursement went through yesterday.

This web page is licenced for your personal, private, non-commercial use only. No automated processing by advertising systems is permitted.

RIPA notice: No consent is given for interception of page transmission.